Scipy has an optimize package that greatly supplement PuLP I tried to conquer the problem of optimizing portfolio, and more concretely to my current workflow – to optimize the weights of a given portfolio.

So the first step is to have a high-level good understanding of Scipy package’s Optimize functions. One can always type “help(scipy.optimize)” for help in command environment.

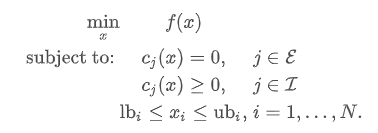

The key focus is Sequential Least SQuares Programming (SLSQP) Algorithm (method=’SLSQP’). It aims to solve kind of problems as such:

An example provided by the official source is as follows:

from scipy.optimize import minimize

def rosen(x):

"""The Rosenbrock function"""

return sum(100.0*(x[1:]-x[:-1]**2.0)**2.0 + (1-x[:-1])**2.0)

# the Rosenbrock function is a non-convex function, introduced by Howard H. Rosenbrock in 1960, which is used as a performance test problem for optimization algorithms.[1] It is also known as Rosenbrock's valley or Rosenbrock's banana function.

# f(x,y)=(a-x)^{2}+b(y-x^{2})^{2}

def rosen_der(x):

xm = x[1:-1]

xm_m1 = x[:-2]

xm_p1 = x[2:]

der = np.zeros_like(x)

der[1:-1] = 200*(xm-xm_m1**2) - 400*(xm_p1 - xm**2)*xm - 2*(1-xm)

der[0] = -400*x[0]*(x[1]-x[0]**2) - 2*(1-x[0])

der[-1] = 200*(x[-1]-x[-2]**2)

return der

ineq_cons = {'type': 'ineq',

'fun' : lambda x: np.array([1 - x[0] - 2*x[1],

1 - x[0]**2 - x[1],

1 - x[0]**2 + x[1]]),

'jac' : lambda x: np.array([[-1.0, -2.0],

[-2*x[0], -1.0],

[-2*x[0], 1.0]])}

eq_cons = {'type': 'eq',

'fun' : lambda x: np.array([2*x[0] + x[1] - 1]),

'jac' : lambda x: np.array([2.0, 1.0])}

from scipy.optimize import Bounds

bounds = Bounds([0, -0.5], [1.0, 2.0])

x0 = np.array([0.5, 0])

res = minimize(rosen, x0, method='SLSQP', jac=rosen_der,

constraints=[eq_cons, ineq_cons], options={'ftol': 1e-9, 'disp': True},

bounds=bounds)

# Optimization terminated successfully (Exit mode 0)

# Current function value: 0.34271757499419825

# Iterations: 4

# Function evaluations: 5

# Gradient evaluations: 4

# from Vijay, who already put the weights optimization functions using scipy, I can reference direclty:

from scipy.optimize import minimize

def portfolio_vol(weights, covmat):

"""

Computes the vol of a portfolio from a covariance matrix and constituent weights

weights are a numpy array or N x 1 maxtrix and covmat is an N x N matrix

"""

return (weights.T @ covmat @ weights)**0.5

def minimize_vol(target_return, er, cov):

"""

Returns the optimal weights that achieve the target return

given a set of expected returns and a covariance matrix

"""

n = er.shape[0]

init_guess = np.repeat(1/n, n)

bounds = ((0.0, 1.0),) * n # an N-tuple of 2-tuples!

# construct the constraints

weights_sum_to_1 = {'type': 'eq',

'fun': lambda weights: np.sum(weights) - 1

}

return_is_target = {'type': 'eq',

'args': (er,),

'fun': lambda weights, er: target_return - portfolio_return(weights,er)

}

weights = minimize(portfolio_vol, init_guess,

args=(cov,), method='SLSQP',

options={'disp': False},

constraints=(weights_sum_to_1,return_is_target),

bounds=bounds)

return weights.x